Performance Bonus Representation. Bonus system. When a paper confirmation of the reasons for the promotion is required

In many large companies workers receive a salary that is equal to or slightly higher than the minimum wage, and they also receive bonuses, and their size can significantly exceed wages. Such bonuses are monthly, and information about them is entered into the employment contract. But in addition, for various reasons, the employer can assign one-time bonuses to his employees. Usually, such funds are transferred if there is a compelling reason.

Nuances of awarding

Standard monthly bonuses act as part of the salary, therefore they are included in the remuneration system on the basis of Art. 135 TC. Additionally, the head of the company can appoint one-time bonuses under Art. 191 TC, which are not included in the salary. Usually, funds are only paid to employees who have distinguished themselves in some way at work, so they should be rewarded.

The rules and procedure for transferring a one-time bonus to employees should be fixed in the internal documentation of the enterprise.

When are funds disbursed?

One-time bonuses are awarded when there are compelling reasons, therefore, they are most often listed in the following situations:

- an employee has increased labor productivity;

- due to the active work of the citizen, the number of buyers in the store has increased;

- a production specialist has increased the competitiveness or quality of the products being created;

- bonuses are paid before holidays or various significant events in the life of employees.

The decision on the appointment of such a payment is made only by the head of the enterprise, therefore this is not his direct responsibility. Often, funds are completely assigned to employees who replaced other employees, performed actions not provided for by their job descriptions, or were engaged in optimizing business processes in the company.

How is it profitable to pay one-time transfers?

The payment of one-time bonuses is considered to be more beneficial for employers than an increase in the salary of employees. This is due to the following reasons:

- enumeration additional premiums is carried out only after the adoption of the appropriate decision by the head of the enterprise, therefore, if the director decides to deprive specific specialist this payment, then it is impossible to challenge such a decision;

- it is allowed to transfer such funds not within a strictly established time frame, but with a certain delay;

- the term for the payment of such funds is not strictly established, therefore, violations of the terms do not fall under Art. 136 TC;

- if necessary, the head of the company can reduce the payroll, denying all employees a bonus.

But the transfer of premiums must be economically justified. Therefore, the head of the company must determine in advance the reason for calculating this amount. Most often, for this, economic reasons are used, represented by an increase in the company's income or the onset of a festive event for the enterprise.

Conditions for payment of funds

The accrual of a one-time bonus is possible only if certain conditions are met, which are regulated not only by law, but also by internal local acts companies. Most often, the basic conditions are prescribed in the collective employment contract or in the provision on bonuses.

The main such conditions include:

- if the director decides to pay funds to the employee from the retained profit of the organization, then he must make such a decision officially, for which a meeting of shareholders is held, a protocol is drawn up and the decision is approved;

- often in the internal documentation of the company, it is indicated that it is necessary to transfer bonuses to employees for length of service or when new modern equipment is put into operation;

- it is not required to indicate the amount of the lump sum payment in the employment contract of each employee.

Other conditions depend on the decision made by the management of the company.

What are the requirements?

Before paying a one-time bonus, the director of the company must take into account some restrictions:

- if the company has a trade union, then it is required to agree with its members all provisions related to bonuses;

- it is allowed to increase payments, but not decrease, if they are enshrined in the employment contract;

- if the head of the company decides on the appointment of payments to employees, then the accountant of the organization must draw up a special certificate, and the head issues an official order.

The amount of additional payments may differ slightly for different employees. The manager independently determines which of the employees will receive this or that payment at a certain point in time.

What documents are being prepared?

Vacation and one-time bonuses, as well as other payments to employees, must be officially recorded in the organization's documentation. Only in this case they will be taken into account in taxation. If the employer prefers to pay employees one-time bonuses for various reasons, then the following documents must be drawn up for them:

- information on bonuses is entered into the collective labor agreement;

- information on the accrual of these bonuses is entered into individual labor agreements, drawn up separately with each employee;

- regulation on remuneration;

- the provision on bonuses, containing information on bonuses paid on a monthly basis;

- provision on one-time transfers that can be transferred for length of service, paid for holidays or appointed for other reasons.

Only with the correct design of one-time bonuses for holidays or other significant events can they be used to reduce the tax base for income tax.

Rules for drawing up a provision on bonuses

Before paying a one-time bonus, the head of the company must correctly draw up its accrual. For this, a corresponding provision on bonuses is formed. It reflects the firm's actual practice in relation to the transfer of bonuses to employees. This document contains the following information:

- it is prescribed that additional funds are transferred to employees only when certain goals are achieved, for example, when sales or the number of buyers increase, when a holiday event occurs, or under other conditions;

- lists the evaluation criteria and conditions for calculating the premium;

- the amount of the payment is indicated;

- lists all employees of the company who can count on these funds to achieve specific goals.

The amount paid can be a lump sum or a percentage of salary. Each company can use its own unique indicators, taking into account the specifics of its activities. The regulation may include other conditions or information, which depend on the area in which the company operates, how many employees work in it, and what is the average earnings of employees.

One-time bonuses are assigned only on the basis of the regulation. An example of such a provision can be examined below.

Consequences of drawing up a regulation

A one-time production bonus in 6-NDFL is reflected only when it is officially issued. Otherwise, the payment is a gift if its size does not exceed 4 thousand rubles.

If the manager draws up a provision on bonuses, then he has the obligation to pay these funds to the employees of the company. Employees, if necessary, can require the manager to transfer this money. Therefore, information is usually entered into the document, which makes it possible, if necessary, to refuse hired specialists in funds.

Are premiums paid?

Taxes are paid on a one-time bonus only if it is correctly issued. Insurance premiums are paid by the employer from this amount, regardless of whether it is included in expenses when calculating income tax. Therefore, the employer will not be able to save on these contributions.

If a citizen works in joint stock company, then the founders have the right to transfer funds from retained earnings. In this case, they will have to hold a meeting of shareholders, as well as formally make a decision. This method of transferring the premium does not reduce the taxable profit of the company.

Thirteenth Salary Concept

In many companies there is such a thing as the thirteenth salary. It is paid at the end of the year as an incentive to employees if the necessary funds are available in the wage fund. It is a one-time payment, since the head of the company cannot be sure that at the end of the year there will be enough funds in the fund to transfer the thirteenth salary to all employees of the enterprise.

There is no information in the legislation on how to correctly transfer to hired specialists this prize... Therefore, company leaders pay it to their employees only if they wish and financial capacity... The accountant of a company cannot carry out such a payment as a monthly salary, so it acts only as an addition to earnings.

In many companies, the thirteenth salary is enshrined in internal regulatory documents. The employer determines when exactly the funds are transferred to the employees, as well as what is the procedure for payment. Most often, this information is included in the provision on bonuses. If such a payment is made out as a one-time bonus, then the head of the company can independently choose the employees to whom the funds will be transferred.

Rules for issuing an order

Accounting for one-time bonuses implies the need for them correct design... If the employer decides to transfer these funds to one or more employees, then he must correctly draw up it by issuing an appropriate order. When forming of this document the following points are taken into account:

- the order contains information about when and in what amount the bonus is transferred to a specific employee or several employees of the enterprise;

- if there are hired specialists of the company who are not entitled to payments, then they are simply not included in this order;

- if an employee who does not receive an award tries to challenge the decision of the management, for which he submits a complaint to the labor inspectorate, then the manager must refer to the content of the bonus provision;

- the order is drawn up in the form No. T-11, if funds are paid to only one employee who in some way distinguished himself before the management of the company;

- if payments are assigned to several employees of the enterprise, then form No. T-11a is selected.

Directly in the order, the head of the company indicates for what reason these one-time payments are assigned. The code of income of a one-time bonus is given, and it is also indicated when exactly the funds will be paid to employees. The employer independently decides in what form the money will be allocated. They can be issued in cash through the company's cashier. If the company's employees receive their salaries to a bank account, then usually bonuses are transferred to this account.

Are taxes levied on payments?

One-time bonus payments are not regulated in the same way as regular incentive transfers. But from them, personal income tax is paid without fail, if they are correctly drawn up. Additionally, insurance premiums are transferred from them.

For the correct calculation and payment of personal income tax, the following requirements are taken into account:

- the possibility of transferring one-time payments is provided for by the content of the company's internal regulations;

- only payments are applied to accounting, which are assigned for any services to the company, and are not tied to weekends or other events;

- all costs associated with paying taxes are certainly recorded in the accounting of the company.

Personal income tax from a one-time bonus is paid by the direct employer acting as a tax agent for its employees.

Other important nuances

Before calculating a one-time bonus, the employer must take into account some significant features. These include:

- if a bonus is paid upon dismissal of an employee, then personal income tax is collected from it on general terms;

- if funds are transferred for holidays or other significant events, then they are not related to professional activities employees, therefore, such expenses cannot reduce the tax base for corporate income tax;

- Unified agricultural tax is not withheld from such remuneration.

Employers can pay one-time remuneration using various tax systems. It is important to consider whether these payments reduce the tax base.

What wiring are used?

Accountants should be aware of the one-time premium income codes and the transactions used. When transferring these funds, information must be entered into the accounting. For this, wiring D91-2 K70 is used. Based on it, the incentive payment is credited from the company's net profit.

Such quotation can be applied when using any type of profit, which may be current or for a previous tax period. Since such costs are other, then D91-2 is used.

What are the income codes used?

Employees can require the employer to create a 2-NDFL certificate at any time. It is required to solve numerous problems, for example, when applying for a loan or receiving other services. This document contains information about all cash receipts of the employee with an indication of their code. Therefore, the question arises, what is the income code of one-time premiums. The main such codes include:

- Code 2002. It applies if an employee of the company is paid incentives for various achievements in the workplace. They can be provided for by legal requirements, the content of an employment contract or a collective agreement. This code is used when paying bonuses based on the results of a month, quarter or year, as well as when transferring money for completing important tasks or for unique production achievements.

- Code 2003. It is used when rewards are transferred from company revenues or through the use of special purpose money. This code is relevant if the target money of the company is used. Typically, this code is used if a premium is paid for various holiday events or anniversaries. Often, such payments act as material motivation for employees. They are not related to execution job duties employees.

- Code 2000. It is used in a situation where a bonus is assigned for the length of service.

With the help of such codes in the 2-NDFL certificate, you can understand which funds were received by the employee at one time or another. The same code marks a one-time production bonus in 6-NDFL. The company's accountant must competently approach the filling of these documents, since he is responsible for any errors or violations found.

Employer's liability for violations

Often, employees have to deal with the fact that the employer does not pay one-time bonuses, although the need for these transfers is due to internal local acts or a collective agreement. In this case, refusal to pay bonuses is a violation on the part of the director of the company.

Under such conditions, employees can file a complaint with various inspecting government agencies. It is most optimal to write an application to the labor inspectorate. The specialists of this service will conduct an audit, the main purpose of which will be to identify violations of workers' rights by the organization's management. Although the transfer of one-time bonus payments is not subject to the requirements of the law, but if this obligation is enshrined in regulatory documents, then the leader is obliged to follow these standards.

Conclusion

One-time employee bonuses are not part of the salary, so they are assigned to hired specialists only if there are some reasons. Most often they are listed for unusual achievements of employees, as well as for the purpose of reward. Their size is determined by the direct employer.

In order for such payments to be official, they must be properly formalized, for which information about them is entered into the collective agreement, or even the employer forms a special provision on bonuses. The director of the firm must follow the requirements contained in these official documents.

Chapter 6.

ORGANIZATION OF CURRENT AND SIMULTANEOUS PROMOTION OF EMPLOYEES

The essence, goals and principles of bonuses

Workers

Improving results labor activity can be achieved through various methods of influencing workers. The most important among them is the additional material remuneration of personnel for the results of work, called bonuses. The concept of an award (from lat. praemium - award) is used in various fields of activity. Prize Is a measure of reward for special achievements or merit in any field of activity. It is one of the forms of material incentives for workers for high quantitative and qualitative results, such as an increase in labor productivity, the introduction of the achievements of science and technology into production, saving material, labor and energy resources, improving product quality, accuracy in observing technological regimes, maintaining equipment in good condition, etc.

The main purpose of awarding - increasing the efficiency of the enterprise by stimulating the labor activity of the personnel. Bonuses for employees are based on the following principles:

· Fairness and validity of the size and differentiation of premiums;

· Material interest of workers in achieving high final results of labor activity, a combination of individual and collective material interest in the results of work;

· Encouragement of creative initiative, responsibility, achievement of high quality work, products, works and services;

· Simplicity of determining the size of bonus payments;

· Clarity and accessibility for employees' understanding of the relationship between their work efforts and remuneration;

Flexibility - changing the bonus system with changing goals and objectives material incentives;

· Publicity of encouragement as a combination of material and moral incentives to work.

It is inappropriate for one and the same group of workers to be encouraged under numerous bonus systems, since failure to meet indicators for some of them will be compensated for by overfulfillment in others, and the bonus will acquire the character of an average guaranteed additional part of earnings, sharply reducing its stimulating effect.

In modern conditions, the role of the bonus as an element of the organization of wages, a flexible part of earnings, which makes it possible to individualize it depending on the results, quality and efficiency of labor, is increasing.

Development of regulations on bonuses, its main elements

Currently, neither the current labor legislation, nor the centrally issued normative acts regulate the provisions on bonuses to employees in the organization. Along with this, in accordance with Art. 144 of the Labor Code of the Russian Federation, the employer has the right to establish various bonus systems that stimulate additional payments and allowances, taking into account the opinion of the representative body of employees. These systems can also be established by a collective agreement.

As a rule, the leaders of the internal production departments are engaged in the development of provisions on bonuses. This allows you to take into account the peculiarities of production activities, the tasks facing the division, the specifics of the forms and systems of remuneration used. The developed regulations are adopted after agreement with the head of the enterprise and with the trade union committee, which ensures their compliance with the goals of the enterprise and the requirements of social protection of workers. Bonus provisions should be reviewed when a new collective agreement is concluded. This allows them to be adjusted in accordance with changes in the production and financial activities of the enterprise, the emergence of new guidelines when stimulating the labor activity of workers.

The main elements of the bonus system, which are reflected in the provision on bonuses are: indicators and conditions of bonuses; sources of premium payments. The statute on bonuses also provides for the size (scale) and timing of bonuses, as well as the range of employees to be awarded.

Indicators and conditions of bonuses are divided into basic and additional. Choice key indicators is determined by the purpose of the bonus system, their fulfillment, as well as compliance with the basic conditions, are mandatory in order to receive the bonus. If the main indicators and conditions are not met, the premium is not charged. Additional indicators and conditions to a large extent play the role of “correctors” that do not allow the achievement of the main indicators to be carried out to the detriment of other aspects of the activity. The fulfillment of additional indicators and conditions is the basis for receiving the premium in full, if they are not met, the amount of the premium is reduced.

Bonus indicators can be absolute(expressed in natural, conditionally natural, labor and value units) and relative(coefficients, percentages, indices).

It is important to divide the bonus indicators into quantitative and qualitative. TO quantitative indicators bonuses include: fulfillment and overfulfillment of production targets for product output and increase in labor productivity, the introduction of technically sound norms and standards, etc. Qualitative indicators reflect not only an improvement in the quality of products, but also positive changes related to other technical and economic indicators of the enterprise. These indicators include: a decrease in the labor intensity of products, savings in comparison with the established norms of raw materials, materials, fuel, tools and others material values; reduction of standardized losses of raw materials, fuel, energy, labor quality coefficient. If qualitative indicators of bonuses are accepted in the bonus system, then the conditions for the operation of this system should be quantitative characteristics. Conversely, if the indicators of bonuses are quantitative, then the conditions of the bonus system should reflect the requirements for achieving an appropriate level of quality.

The main sources of premium payments are the wage fund, enterprise profit, savings in working capital, raw materials, materials, fuel, energy.

Bonus scales link the fulfillment or non-fulfillment of specific indicators and conditions with the amount (percentage) of the premium, or the amount of its increase-decrease.

The circle of bonuses determines the categories of employees who are encouraged under this bonus system.

In accordance with this goal, various classifications of awards and premium systems are used. So, depending on the number of indicators used in the incentive system and the conditions of bonuses, they distinguish simple and complex systems, depending on the use of the incentive system in relation to individual employees or their group - individual and group.

The provision on bonuses can be developed for the enterprise and its structural divisions, as well as for selected categories workers, positions, professions, qualification groups individual professions. Bonuses can be paid at different intervals: for a month, quarter, six months, a year, which depends on the specifics of the organization of production and labor, current accounting and reporting.

The development of the Regulations on Bonuses involves the establishment of short-term, medium-term, long-term or special goals. The set goals are achieved by using the following bonus systems: for the main results of activities, one-time bonuses, special bonus systems. Bonuses for the main results of activities are called current, payments are made monthly, one-time bonuses - one-time, providing for payment at the end of the year. Special bonus systems take into account the result of activities aimed at saving specific types of material resources, creating and implementing new technology, technology, design changes and technical characteristics, as well as the time to achieve this result.

The efficiency of the enterprise, its ability to respond quickly to changing market conditions and competitiveness to a significant extent depends on the degree of validity of the chosen system.

· Indicators of bonuses should be focused on solving the problems of the enterprise;

· It is necessary to evaluate the indicators of bonuses, providing a higher remuneration for work of greater tension;

· The number of indicators and conditions of bonuses, as a rule, should not exceed three;

· There should be no contradictions between indicators and conditions of bonuses;

· The method of determining the premium and the scale of bonuses should be fairly simple;

· The intensity of the indicators of bonuses should be periodically checked;

· The circle of employees to be rewarded should be determined by their influence on the indicators of bonuses;

· The frequency of bonuses should constantly stimulate employees to improve their performance;

· Sources of payment of bonuses must correspond to indicators and sources of bonuses and fully meet the need for financial resources necessary for the payment of bonuses;

· The bonus system should be economically justified, which is confirmed by an assessment of the effectiveness of its application.

When developing provisions for bonuses, it seems appropriate to lay in them the three-stage principle, widespread in enterprises of countries with developed market economy, according to which it is necessary:

1) at the first stage, accrue bonuses for the performance of indicators that characterize the activities of the entire enterprise;

2) at the second stage at the level of structural divisions, when giving bonuses, use specific indicators that characterize their activities: for accounting - the performance of their official duties at a highly professional level, which consists in minimizing taxes from the enterprise; for the sales department - fulfillment of the receipt plan Money to the current account of the company; for the transport department - fulfillment of the plan for the dispatch of goods, etc.;

3) at the third stage, use bonuses for the performance of individual indicators that characterize the efficiency of the labor activity of an individual employee.

Bonuses are one of the most flexible elements that form employee remuneration. Unlike tariff rates and official salaries, the bonus is not a guaranteed payment, its size can vary significantly depending on many factors. The premium will have the strongest impact if the following requirements:

· Employees must have timely and comprehensive information about the indicators and conditions of bonuses, as well as other aspects of the bonus system;

· A clear focus on the results that the organization wants to achieve using one or another bonus system is necessary, in the presence of an easy-to-understand relationship between these results and the received remuneration;

Indicators and conditions of bonuses must be in full compliance with the requirements of the legal framework and conditions of technological process subject to safety regulations, sanitary and hygienic norms and standards.

The practice of enterprises shows that the bonus is established, as a rule, not only in accordance with the results of the employee's work, but also taking into account the duration of his continuous work experience at this enterprise therefore, the bonus and remuneration regulations in force in the enterprise must be in full compliance.

The bonus system can have several provisions O bonuses. The provisions relating to one bonus system contain elements that reflect its principal features. The content of the provisions on bonuses is determined by the specific tasks and conditions of labor incentives.

Sales GeneratorReading time: 10 minutes

We will send the material to you on:

In this article, you will learn:

- Why introduce bonuses to employees

- What is the bonus system

- What indicators can you rely on in employee bonuses?

- How to document the bonus system in the organization

- How to apply for a one-time bonus

- What mistakes do enterprises make when developing a bonus system?

Bonuses for employees - effective method motivate to work more productively. Knowing about the opportunity to receive financial incentives, employees work with high efficiency, more fruitful and efficient, improve their qualifications and competence. But how to organize the awarding process competently and fairly? About it – in our article.

The main purpose of remuneration and bonuses for employees

Bonuses to employees are the main method of increasing their interest in improving their work performance. If the company operates a bonus payment system, then the calculation of the final amounts is formed according to a special scheme. The main part of earnings is payment at the wage rate, piecework system or official salary. In addition to this part, additional payments are made to the staff for high performance indicators.

An award in the general sense (from Lat. Praemium - a reward) is a monetary or other material incentive given to an employee for success in a particular activity as a reward.

At the enterprise, a bonus is called a part of the salary focused on motivating personnel to improve the quantitative and qualitative performance criteria. Thanks to bonuses, issues in the economic sphere and in the field of management are solved much more efficiently.

Bonuses to employees for performance results are introduced, first of all, to increase the efficiency of the labor process by encouraging personnel to more actively perform their functions.

Types of employee bonuses: a brief classification

The diagram below shows an example of the types of bonuses for employees.

Awards are:

- production. They are issued if employees fully solve production problems and do an excellent job with their official duties... Production bonuses are systematic. That is, companies can make payments every month, every quarter, or at the end of the year;

- encouraging. Such bonuses do not directly relate to the performance of the employee's official duties.

Payments are made at a time:

- At the end of the year, based on the results achieved;

- Every year for seniority;

- Bonuses are given to employees with high rates labor;

- The payment of bonuses is tied to memorable dates, anniversaries, etc.

By form of payment bonuses are:

- monetary;

- commercial (we are talking about memorable gifts, for example, personalized watches, sets of stationery, household appliances, various certificates).

Depending on the evaluation of indicators the results of labor bonuses to employees of the company are:

- individual - the bonus is accrued to one or several employees, taking into account their personal contribution to the activities of the enterprise;

- collective - the award is given to all personnel for achievements in labor activity. Such payments are calculated based on the collective performance of a department or company in general. Further, the received amount is distributed among the employees, depending on their personal contribution. Personal contribution is determined, taking into account the hours worked, basic wages and the coefficient of labor participation.

By methods of accrual awards can be:

- absolute, which are paid in a fixed amount;

- relative, calculated as a percentage.

By frequency distinguish between:

- systematic bonuses, which are made on a regular basis;

- one-time bonuses. That is, the company financially rewards employees, for example, for solving a problem of increased complexity.

The frequency of payment of premiums depends on several factors, these are:

- The peculiarity of the activities of the enterprise, its departments or specific employees;

- The nature of the bonus indicators;

- Accounting for labor results for certain periods of time.

By intended purpose bonuses are:

- general, when awards are given for success in work;

- special, when employees are rewarded for solving specific problems.

The employee bonus system and its main elements

Any organization has its own procedure for awarding employees, regulated by local documents. This is a bonus system for personnel. There are also criteria and indicators for bonuses to employees. These are elements of the incentive payment system that determine how, to whom, and in what volume the bonuses should be awarded.

Elements of the employee bonus system are:

- bonus criteria for employees - indicators that must be met by personnel in order to accrue monetary remuneration;

- a list of employees who are entitled to receive a bonus;

- the procedure for calculating premiums;

- procedure, timing of accrual and issuance of bonuses;

- sources of premiums;

- procedure and grounds for reducing the amount of bonuses.

Since there are no clear requirements regarding the list of elements of the bonus system at the legislative level, each company determines them at its own discretion.

Let's dwell on the existing bonus systems:

- Bonuses for current activities.

- Project bonuses.

- Bonus programs.

- Loyalty awards for the company.

- Bonuses as part of the management system.

This system is similar to the traditional monthly payroll scheme. That is, if an employee works well, without comments, then he is given bonuses monthly. Typically, the incentive payment is a certain percentage of the salary. This type of bonus is very much in demand, since it increases the motivation of workers to work and is quite simple to calculate.

The most visual bonus model. If an employee performs a predetermined amount of work, then he receives a bonus. The amount of the bonus is reported to him before the solution of the assigned tasks.

The amount here depends on the percentage that the manager is willing to pay to employees. It is he who sets the amount of funds planned for issuance. This value depends, as a rule, on the personal interest of the employer in the allocation of a specific amount for the payment of bonuses. This type of incentive is effective if the company attaches great importance to group work, when employees of departments perform similar labor functions.

As an example, here we can cite the usual thirteenth salary that companies give out to personnel under New Year... It is difficult to say for what such bonuses are paid, but this phenomenon has already become a tradition.

The largest Russian company for the production of baby food was thinking how to increase productivity. As a result, it was decided to pay bonuses to the staff in case of successful implementation of the proposals.

Bonuses are also classified on an accrual basis. Some companies form bonuses from top to bottom, creating a bonus fund based on additional profit. Others build the scheme from the bottom up, that is, they immediately put the issuance of incentive amounts into the budget as part of the payroll.

Each company strives to create a flexible and universal bonus system.

Principles of bonuses to employees of the enterprise

There are special principles of bonuses:

- fair and reasonable premiums;

- financial interest of employees in achieving the set results;

- general collective interest in work;

- encouraging creative approaches to activities, responsibility, the desire to produce quality goods and services;

- simple determination of the amount of the bonus;

- clear and clear understanding of the ratio by employees labor practice and financial incentives;

- flexible changes in the concept of bonuses in accordance with the new goals and objectives of the material incentive;

- publicity of the premium concept as a combination of material and moral incentives in work.

The criteria for rewarding employees should correspond to the types of production tasks, depending on what kind of labor contribution to the development of the company was made by each employee and the entire team as a whole. There should be very few criteria. At the same time, it is necessary that there are enough of them to ensure the connection between the incentive and the main production goals with the results of the work of hired personnel.

Indicators of bonuses to employees: whom and for what to reward

To justify the accrual of bonuses, it is necessary to clearly formulate the indicators of bonuses to employees of the enterprise. There are indicators:

- quantitative (fulfillment and overfulfillment of the planned volume, the percentage of fulfillment of the production standards, ensuring the uninterrupted and rhythmic functioning of the equipment, compliance or reduction of the planned terms of repair measures, carrying out work in a smaller number in comparison with the norm, etc.);

- high-quality (improving the quality of manufactured goods (works) and other technical and economic indicators of the company's activities (workshop, site, shift, team), including a decrease in the labor intensity of goods, savings in comparison with the established consumption rates of raw materials, materials, fuel, tools and others material assets, reduction of standard losses of raw materials, fuel, energy).

The criteria for awarding bonuses to employees are:

- Execution / overfulfillment of planned works for the release of goods, provision of services;

- Clear and complete adherence to requirements job descriptions and labor agreements from employees;

- Saving of enterprise resources by employees in the course of work;

- Conclusion of a certain number of contracts for a set period of time: month, quarter, year;

- Employee absence disciplinary action for a specific time period;

- Compliance with the norms and rules of labor protection;

- Exhaustive execution of applications of local acts of the enterprise;

- No defective released goods;

- Lack of substantiated complaints from the company's customers.

Bonuses to managers, specialists and employees are calculated based on criteria related primarily to making a profit.

Among the criteria for awarding executives are:

- the efficiency of the entire enterprise (for the head) or the structural department (for the heads of the structural divisions);

- the amount of work performed by personnel under the guidance of a specific boss;

- the absence or minimum number of defective goods at the sites entrusted to the managers;

- adherence to job descriptions and provisions of labor agreements on the part of employees;

- the conclusion by the chief or employees in his subordination of contracts beneficial for the enterprise;

- solution of important tasks related, for example, to the organization of personnel training.

The company must clearly list the criteria for bonuses, differentiate them by groups of employees and departments. It is possible that a single bonus criterion will turn out.

The amount of bonuses is set in accordance with each bonus indicator or as a percentage of the basic salary, or in a fixed amount of money. So, for an increase in production volumes, an improvement in productivity, a decrease in the cost of goods or an improvement in the quality of products (work, services), the amount of the bonus is assigned as a percentage for each measurable point of improvement of the corresponding indicator in comparison with its norm, planned or other value.

Each company issues bonuses to its personnel at different intervals. Bonuses to employees in this regard are determined by the production characteristics and the nature of the enterprise's labor activity, the duration of the production cycle and the conditions for calculating bonuses, the frequency of planning, accounting and reporting established for them. Staff bonuses are usually given every month.

Why document the conditions for bonus payments to employees

The Labor Code of the Russian Federation says that the employer has the right to assign a bonus to his employees, but he is not obliged to do this. That is, the manager, at his own discretion, decides the issue of approving a remuneration system that provides bonuses. The mechanism of remuneration can be piece-rate bonuses, salary bonuses, etc. This fact must be recorded in local acts.

Important! If the internal documentation of the enterprise reflects the remuneration system, which includes bonuses, then the employer in this case is obliged to calculate and issue bonuses to his personnel in accordance with internal agreements. If he does not fulfill this obligation, workers can contact the labor inspectorate. That is why it is important to correctly reflect in the documents the procedure and conditions for issuing awards.

We list the documentation in which the conditions and procedure for awarding bonuses to employees should be spelled out:

- Employment agreement with the employee.

The employment contract should indicate the conditions for the payment of wages and additional financial incentives, including bonuses (Art.57 Labor Code RF). It should be unambiguously clear from the text of the document when an employee has the right to count on bonuses and to what extent.

The term for bonuses in the employment agreement can be reflected in two ways: fully indicate the circumstances and procedure for issuing bonuses or refer to the internal regulations of the enterprise, where this information is spelled out.

It is better to give preference to the second option and mark the name of the local documentation in the text of the agreement. It's easier and more convenient. If it is necessary to change the conditions of bonuses, then it will only be necessary to reflect this in these internal documents, and not in each agreement.

- Regulations on remuneration, regulations on bonuses.

Here the managers indicate all the significant conditions for bonuses:

- the possibility of financial incentives for employees (remuneration system);

- the types of bonuses existing in the company, and how often they should be paid (for the results of activities during a month, quarter, year, or, for example, a one-time bonus on the eve of holidays, etc.);

- list of employees to be rewarded (all personnel, specific departments, selected positions);

- specific indicators and scheme for calculating bonuses (for example, a certain percentage of salary for fulfilling a sales plan; a fixed amount for specific holidays, etc.);

- other conditions established by the management. The main thing is that there are no inconsistencies between the conditions of accrual and the issuance of bonuses. It should clearly follow from the conditions when and to what extent the management is obliged to reward the staff of their institution.

- Collective agreement.

If a collective labor agreement is concluded between the employer and employees, then it must also contain information on the procedure for calculating and issuing bonuses.

Note: the employee must sign the employment contract, as well as leave a signature in the regulation on remuneration, in the regulation on bonuses and in collective agreement(if any) after review. These documents are provided to the employee by the manager.

Regulations on bonuses for employees

Regulations on bonuses - an internal document of the enterprise, where all the rules for bonus payments are spelled out. The employee bonus regulation, a sample of which you can download on the Internet, has an important advantage. Tax office will not be able to present the company with claims related to the inclusion of bonuses in the composition of labor costs when calculating income tax.

The regulation on bonuses for employees (2018) can be presented in the form:

- Section (appendix) of the collective agreement;

- Section of the regulation on remuneration;

- An independent normative act.

If the company is small, it is allowed to draw up a single provision on bonuses. If the firm is quite large, it is better to develop a statement for each division or group of departments.

The structure of this document is always the same. It prescribes the criteria and conditions for issuing bonuses, the amount and frequency of their payment, the calculation scheme, a list of violations due to which the premium is reduced, as well as a list of payments for which bonuses are not charged. It is recommended to include the following chapters in the provision on bonuses for employees, which you can download on the Internet:

Chapter 1. General Provisions.

In this section, the goals of introducing the bonus system are prescribed. Let's say that monetary incentives can be aimed at increasing labor productivity or the quality of goods, works and services.

Chapter 2. Types of bonuses and conditions of bonuses. It is better to reflect in the document what the award is for and by what criteria it is paid. Thus, bonuses may be due for:

- the intensity of labor activity;

- continuous work experience at the enterprise;

- results of labor activity.

Important! To justify the accrual of bonuses without any problems, it is necessary to develop and clearly formulate the criteria for bonuses to employees.

You should not use vague wording, for example, "for conscientious work" or "observance of labor discipline."

Here you can also mention the bonuses for the holidays and other rewards paid out of profits. In general, bonuses may differ depending on:

- categories of employees: for example, bonuses are awarded only to workers, bosses, specialists or employees (used to assess the results of production activities) or to all personnel (for example, bonuses for length of service or for general achievements in work);

- time of payments (based on the results of work for a month, quarter or year);

- frequency of issue (bonuses are both regular and one-time);

- the fund from which the funds are taken for the issuance of bonuses (from the wages or profit fund);

- relationship to taxation (whether bonuses are taken into account for tax purposes or not);

- the amount of premiums (fixed or as a percentage of some indicator).

Chapter 3. The procedure for calculating bonuses.

This chapter establishes a list of employees who are entitled to bonuses. Prescribe the names of departments, specialties, positions or types of work.

The amount of the bonus can be expressed in a specific amount, as well as as a percentage of a specific indicator. For the full implementation of the plan, the manufacture of products in the prescribed volume, the absence of defective products, complaints, the performance of work and the provision of services at a given time, etc. part of the salary).

If it is difficult to determine the amount of incentive payments due to the large number of bonus criteria, it is better to set the minimum and maximum amount of bonuses (for example, the amount of the monthly bonus is from 10 to 40% of the salary). Often, department heads are tasked with setting the amount of bonuses for a particular employee. But in such situations, managers can be accused of bias. Therefore, it is better if the amount of the premium is nevertheless related to specific criteria.

In addition, the chapter should describe the scheme for making a decision on the accrual of bonuses:

- Who decides to reward employees;

- How this decision is brought to the accounting department;

- How often a given bonus is given to employees;

- How long does it take to make a decision on staff bonuses based on the results of a month or quarter.

It also indicates the conditions due to which the management has the right to reduce the amount of the bonus:

- the employee does not perform or improperly performs his labor functions;

- violates the internal work schedule;

- violates labor discipline (skips, appears at work in a state of alcoholic, narcotic, toxic intoxication, etc.);

- does not follow orders from superiors;

- violates the requirements of labor protection and industrial sanitation.

Chapter 4. Types of violations that reduce the amount of bonuses.

This chapter prescribes the conditions for issuing premiums, as well as a list of situations due to which the premium is reduced or not assigned:

- the employee was transferred to a position with a lower pay, he was reprimanded or reprimanded;

- employee violated fire safety and safety precautions, labor protection requirements, internal labor regulations;

- poorly performed their labor functions prescribed in the job description, ignored their duties or performed them in an inappropriate manner;

- did not follow the orders and orders of the management or the requirements of other administrative documents of the company;

- lost, damaged, caused damage to the property of the enterprise or other loss by his actions;

- skipped weekdays, showed up at work in a state of alcoholic intoxication, or was absent for no good reason.

Chapter 5. Conclusion.

The chapter indicates how the regulation comes into force and how long it is valid.

The moment of entry into force can be reflected in the document itself or in the order of the head of the enterprise. If the period of validity of the regulation is not indicated, it is considered that it is unlimited. That is, the provision is relevant until it is canceled or until the moment when the company adopts a new internal act, which prescribes the procedure for awarding bonuses to employees.

How to issue a memo and an order for bonus payments to an employee

Regular bonuses provided by the wage system do not need to be fixed separate documents so that decisions on the issuance of such a reward can be made. The procedure for incentive payments is already reflected in the internal statutory act on bonuses.

If the manager wants to issue an unplanned bonus to a specific employee, thus noting his merits, and this financial incentive is not provided for by a collective or labor agreement, he can apply to higher authorities for a this decision... In this case, a memo is drawn up (bonuses for employees). The main part of its content is information about the basis for the question of employee bonuses.

The final decision on both regular and one-time bonuses is made by the director of the enterprise. But in the first case, he asserts the results of the distribution bonus fund the company, and in the second - decides whether it is worth rewarding the employee or not.

The service record of the employee's bonus includes the following information:

- The name of the company (in full) where the employee works;

- FULL NAME. general director institutions and the direct manager of the employee in relation to whom the question of bonuses has arisen;

- General information about the specialist, his work experience, a list of successes and achievements in work;

- Description specific situation, according to the results of which it was decided to reward this employee (for example, he overfulfilled the plan, developed and implemented a rationalization idea, etc.);

- Prize application;

- Date of preparation memo.

The head of the unit where the employee to be awarded is obliged to familiarize himself with the memorandum and sign it. If an employee has several managers of different levels, then all of them must sign the document.

After the approval of the application for bonuses (the visa of the director of the enterprise is used as confirmation on the form of a memo), the personnel department forms an order for bonuses to employees, a sample of which must be in each organization. The order must also be signed by the head of the company. When all the paperwork is completed, the accountant issues a bonus to the employee.

To issue a bonus order, you can fill in:

- unified forms T-11 and T-11a, approved by the decree of the State Statistics Committee of the Russian Federation of 01/05/2004 No. 1;

- free form. It must be developed and approved by a specific company.

In either case, the order will have legal force, since from October 1, 2013, it is allowed to use not only unified forms for drawing up this document (see the data of the RF Ministry of Finance 04.12.2012 No. PZ-10/2012, section “Forms of primary accounting documents ").

But the order form must still contain the information necessary for such documentation (see clause 2 of article 9 of the Federal Law "On Accounting" dated 06.12.2011 No. 402-FZ), namely:

- Title of the document;

- the date of its formation;

- the name of the institution;

- the size and unit of measurement of the premium (for example, a cash bonus in the amount of RUB 10,000, etc.). In this case, it is necessary to register:

- Full name of the employee to be awarded;

- the name of his position and the corresponding structural department;

- basis for bonuses;

- form of encouragement;

- the size of the bonus;

- according to whose idea the bonus is being awarded;

- job title, full name and signature official responsible for the execution and / or registration of the operation / event;

- the signature of the director of the enterprise.

Rostrud's letter dated February 14, 2013 No. PG / 1487-6-1 says that non-governmental institutions have the right to use free forms of primary accounting documentation containing the above data.

Evaluation of the effectiveness of the employee bonus system

In order for the employee bonus system to be effective and function successfully, it must be regularly analyzed and monitored. If errors are detected and eliminated at every stage in a timely manner, then both an individual employee and the entire company will work much more efficiently.

In short, an effective incentive system provides visible economic benefits that exceed the cost of its implementation. Moreover, each employee receives an appropriate financial reward for his work.

The main criteria by which the bonus system is assessed are:

- compliance of the indicators taken into account when awarding bonuses to the goals of the department or enterprise in general;

- assessment of how correctly the basis for the calculation has been chosen. It is necessary to regularly analyze the degree of implementation of the selected system of indicators over a long period of time. If the established baseline is below the actual level of its implementation on a regular basis, it needs to be revised;

- the presence of positive dynamics of the estimated indicator from the introduction of the bonus system. If the incentive scheme does not contribute to the improvement of the specified labor indicators, then it has exhausted itself, and therefore you need to think about introducing a different mechanism. In this case, the influence of factors that do not depend on the will of the employee should be excluded (malfunctions technical means forced downtime);

- the adequacy of the amount of the bonus. The amount of the bonus must exactly match the achievements of the employee. It is rather difficult to assess this, since it is necessary to analyze the impact of numerous factors. If several bonus factors are established, you need to find out if there are any imbalances in the labor costs required for their implementation. It should be understood that bonuses in the amount of 7% or 10% of the salary, the tariff rate are not incentive;

Application

PROCEDURE FOR CREATING AND USING MAPS OF INDICATORS FOR ASSESSING LABOR RESULTS FOR A SPECIFIC PERIOD

Glossary of basic terms

Subsidiary units- divisions of the enterprise, the result of which is service maintenance the main divisions of the plant.

Bonus group- a group of positions for which the same bonus conditions are established.

Group indicators- indicators for assessing the effectiveness and efficiency of employees of one structural unit or enterprises as a whole, aimed at measuring the degree of achievement of the general goals set for this group. A group indicator (usually quantitative) is common to all employees in a given group. The share of group indicators in the overall assessment is determined separately for each group of positions.

Performance assessment range- the values of the quantitative indicator (from the minimum to the maximum), within which the amount of the premium is determined.

Individual indicators- indicators for assessing the effectiveness and efficiency of an individual employee, used to measure the degree of achievement of the goals set for him. Individual indicators can be both quantitative and qualitative.

Map of indicators for assessing work results for the position (Further- map of indicators) - a set of indicators corresponding to the key areas of responsibility of a given position, indicating the weight, range of performance assessment, calculation methodology, assessment objects, data sources for calculation.

Qualitative (expert) indicators- indicators designed to assess the performance of an employee in the position held, based on the expert conclusions of several persons (experts). Qualitative indicators are calculated in accordance with the methodology for performing an expert assessment of labor results.

Quantitative data- data on the activities of the company for the period of assessment, expressed in specific units of measurement. Used to calculate quantitative indicators.

Quantitative indicators- indicators reflecting the degree of achievement of the target result; expressed in physical or monetary units, as well as in relative form. The calculation methodology and data sources for quantitative indicators are indicated in individual card indicators for each position.

Assessment object- one of the criteria for expert assessment, a qualitative indicator of labor results. Each object is assessed separately. In the system for assessing the results of the company's labor, two to five objects of assessment are usually used for one expert indicator.

Main divisions- subdivisions of the enterprise, the result of which is the release of marketable products.

Reporting period- the period for which the assessment of labor results is carried out (month, quarter, year).

Assessed- an employee of the company holding a position included in the performance assessment system. His activities in this position for reporting period subject to evaluation.

Evaluator (expert)- an employee of the company, included in the performance assessment system as an expert. Is an internal and / or external client (consumer of labor results) of the evaluated employee.

Indicators for assessing labor results- indicators of the effectiveness and efficiency of an individual employee, divisions and the company as a whole. Performance indicators are divided into group and individual, quantitative and qualitative.

Premium (variable remuneration)- additional remuneration, depending both on the results of work specific employee, and from the achievement of the planned results of the company as a whole.

N-1 level employees- employees directly subordinate to the director of the enterprise.

N-2 level employees- employees directly subordinate to directors in areas.

Employees of level N-3 and below- workers subordinate to lower-level managers and ordinary workers.

The actual value of the indicator- the value of the quantitative indicator for assessing the results of labor for the reporting period, calculated in accordance with the calculation methodology given in the map of indicators.

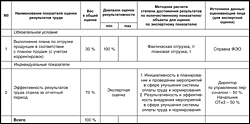

1. Map of indicators for assessing labor results (I)

Agreed:

Head master _____________________

Note:

1. For the main divisions, it is recommended to use two types of group indicators: the indicator of the enterprise and the indicator of the department. For posts at the N-3 level and above, the group score of the enterprise is used, and for posts at the lower levels, the score for the department is used.

In some cases, instead of a group indicator, the parameter “ mandatory conditions", When fulfilling which, the premium for this indicator is not calculated through algorithms, but is set in a specific numerical expression. An example is the bonus card above.

2. An example of the calculation of the premium: suppose the fulfillment of the norms was 125.5%

The amount of the premium, thus, amounted to 12.75%.

For support units, regardless of the level of the position occupied by the employee, the indicator of the entire enterprise is used as a group indicator (or condition).

3. Individual indicators are determined in accordance with the key areas of responsibility of the evaluated employee holding the given position. The weight of each individual indicator should be set in the range of 10-60%. In exceptional cases, for pieceworkers, it is allowed to set the weight of an individual indicator in the range of 10–90%.

4. The range of performance assessment for each quantitative indicator is determined on the basis of statistical data for previous periods. This sample should cover at least four periods. The average value of the sample for the year is taken as the maximum value of the bonus scale.

For a qualitative (expert) indicator, it is necessary to provide assessment objects that reveal its essence. In the performance assessment system, two to five objects of assessment are usually used for each indicator. Also, in the column for this indicator, a list of assessors is provided, indicating the weight of their opinions in the overall assessment.

Map of indicators for assessing labor results (II)

Click image for a larger view

5. The peer review scores can be increased to five or decreased to zero. Experts fill out an expert assessment questionnaire, then an order is issued to increase (decrease) the score.

With an expert assessment of five points, the maximum percentage of the premium for the indicator increases to 29.2%. Thus, with an expert assessment other than three, the percentage of the premium for the indicator is calculated by the formula:

|

Expert review |

|

For example, the employees of the department were given an expert assessment of three points on a five-point scale, then 3: 5 x 29.2% = 17.52%.

6. The bonus card is agreed with the immediate supervisor of the evaluated employee or with the head of the structural unit.

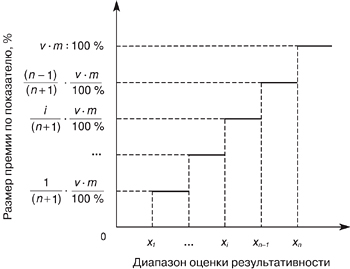

2. Rules for calculating the amount of premium by indicator

The methodology for calculating the amount of the premium for each indicator is given on a separate sheet, as an appendix to a map of indicators for assessing labor results and in accordance with it.

To calculate the amount of a premium based on a quantitative indicator, such a technique can be used. The range of performance assessment is divided into an even number of intervals (usually from 4 to 10) as follows: first, the middle of the performance assessment range and the corresponding average premium for the indicator are determined:

As a result of sequential division of the range, we get the n-th number of intervals:,….

After the range of performance assessment is divided into a finite number of equal intervals, the bonus amount for the indicator is determined according to the following rule:

x n = b and more

Graphically, it can be represented as follows:

Example. The average employee bonus percentage for a certain period is 20%. The weight of the indicator is 30%, the range of performance assessment is 80–120%. In this case, it is advisable to divide the range of performance assessment into four intervals:,,,.

The maximum premium for this indicator will be:

For the gap -

| 2 | NS | 2 x 20% x 30% | = 4,8%. |

For gaps, calculate the premium by analogy with gaps,.

For actual values of the indicator less than 80%, the amount of the premium will be 0%, and over 120% - 12%.

Thus, the amount of the premium in this example is determined according to the following scheme:

3. Appendix to the map of indicators for assessing labor results (I)

Click image for a larger view

Note:

1. To calculate the amount of a premium by a qualitative indicator, it is recommended to use a methodology similar to the method of calculating the amount of a premium by a quantitative indicator.

Graphical representation:

2. The total amount of the premium for the period is calculated as the sum of the actual values of the premium (in percent) for each indicator.

Appendix to the map of indicators for assessing labor results (II)

Click image for a larger view

1. The procedure for calculating the amount of the premium due for the reporting period.

Employees of the department of labor and wages (OTiZ) calculate the amount of bonuses due for the reporting period on the basis of certificates provided by the heads of structural divisions on the implementation of group and individual indicators in the prescribed manner.

Employees of OTiZ communicate information about the actual amount of the bonus (including by indicators) to the immediate supervisor of the employee with the aim of further communicating it to the employees of the enterprise in the prescribed manner.

2. The procedure for revising the cards of indicators for assessing labor results for the reporting period.

The basis for amending a map of indicators for assessing labor results is an:

change in the main functions of the employee (group of employees), in the event of reorganization, changes organizational structure, release of numbers, etc .;

analysis of the degree of achievement of results, carried out by employees of health and safety, identification of indicators for assessing labor results that do not have a stimulating effect on the employee (group of employees) in achieving them (them) higher indicators.

4. The procedure for filing mutual claims and distribution of variable remuneration (bonuses) between labor collectives and employees

The procedure for making Claims and distributing variable remuneration (premium)

1. General Provisions.

This procedure has been developed and is being introduced in order to:

creation of prerequisites and conditions for highly productive work of labor collectives employed at various stages production process, and in different, but interrelated processes (production, provision, service, management);

development of labor rivalry;

increasing the moral and material interest of labor collectives (brigades) and individual workers in achieving high end results.

2.1. A claim is a total expression of wage losses incurred by a team (section, department, service) in the reporting month due to the fault of allied collectives in industrial relations.

2.2. The claim is drawn up according to the principle of its recognition, that is, the presence of mutual consent of labor collectives (the sender and the recipient of the claim) in the form of an Act and is confirmed by the signature of higher managers (sample - Form No. 1).

2.3. The grounds for filing a Claim may be: downtime, accidents, poor product quality, interruptions in supply, etc., which significantly influenced the results of the work of this team for the reporting month.

2.4. The calculation of the amount of wage losses for the submitted Claims is carried out by Health and Safety on the basis of the Act and the data of the relevant departments and services of the enterprise (according to the belonging of functions), confirming the legitimacy of the Claim.

The amount of wage losses is calculated based on the amount of variable remuneration due to the labor collective - the sender of the Claim in the reporting month in accordance with clause 5.2.2. Regulations on the conditions of remuneration and bonuses for employees.

2.5. Submission of a Claim to the labor collective (brigade) about poor-quality performance of work (services) or non-compliance with the requirements in the framework of industrial relations between interconnected teams or teams, is expressed in the redistribution of the premium between the sender and the recipient Claims in the direction of increase or decrease (respectively) are presented in the established below okay.

2.6. To simplify the calculation of the amount of wage losses and the amount of penalties charged for the submitted Claim, the system of labor contribution ratios (KTV) is used, presented in Form number 2 to this Procedure, namely:

at KTV collective< 1,0 (penalties) - as the product of the amount of variable remuneration calculated on the basis of individual performance indicators of the labor collective - recipient Claims for the reporting month as a percentage, the amount of the salaries of this team and the installed cable TV, divided by 100%;

with KTV collective> 1.0- an additional payment is made to the amount of variable remuneration collective - the sender A claim calculated on the basis of individual indicators of his work for the reporting month, which is calculated in the amount of penalties received, but not more than 50% of the amount of variable remuneration due collective - recipient Complaints based on the results of work for the reporting month.

The redistribution of the amount of bonuses between teams, taking into account penalties, is approved by the Director of Human Resources and Social Development.

2.7. The Acts of Mutual Claims drawn up in accordance with the above procedure are provided to the Health and Safety Department for calculating the amount of penalties in the working order, that is, as they are presented (they are not accumulated at the end of the month).

2.8. Within labor collectives, the amount of variable remuneration is redistributed among employees, taking into account the coefficients of their labor efficiency (KET), that is, in proportion to the labor contribution of each employee. KET is established by the direct supervisor of the labor collective (senior foreman, foreman, shift foreman, foreman, etc.) in agreement with the trade union group.

It should be borne in mind that:

KET equal to one, is established for employees who did not have comments from the administration within a month, who completed the production task with high quality, did not violate labor discipline, labor protection rules and other omissions;

KET is below one and to zero it is established for employees who worked less productively and intensively than other members of the team, made defects, violations of technology, labor discipline, labor protection and other omissions;

KET above one to 1.5, as a rule, it is established for employees who have successfully completed all production tasks and tasks of managers; those who have taken the initiative aimed at improving the efficiency of the work of the brigade; those who have achieved high quality work; performed the functions of absent workers; combining professions; successfully performing the most laborious and strenuous work; who have shown high professional skills, etc.

Team leaders - recipients of the Claim are given the right not to submit for bonuses in the reporting month exactly those employees, through whose fault the Claim was received (accidents, defects in work, violation of the technological process, work and job descriptions, etc.).

Form 1

ACT

on the presentation of a Claim to the labor collective

Click image for a larger view

Form 2

SCROLL

claims and the amount of increase and decrease in labor contribution ratios

Tab. 1. An approximate list of increasing indicators in determining the KTV for the team - the sender of the Claim

|

P / p No. |

Name of Claim |

Mean. KTV |

| Increased labor intensity, additional costs of working time due to the fault of subcontractors (other structural divisions) |

from 0.1 to 0.3 |

|

| Additional labor costs to correct defects due to the supply of low-quality raw materials, materials, semi-finished products, etc. |

from 0.1 to 0.5 |

|

| Execution of the most labor-intensive and complex work in comparison with other structural divisions (teams) |

from 0.1 to 0.3 |

|

| Elimination of the consequences of an accident that led to losses in production (non-compliance with production standards due to downtime not through the fault of the team that sent the Claim) |

from 0.1 to 0.3 |

|

| Development and implementation of new projects aimed at increasing production efficiency to compensate for losses |

Tab. 2. An approximate list of decreasing indicators in determining the KTV for the team - the recipient of the Claim

|

P / p No. |

Name of Claim |

Mean. KTV |

| Excessive downtime of site equipment due to the fault of subcontractors (service divisions) for a certain period |

from 0.1 to 0.3 |

|

| Violation of technological discipline, requirements of standards |

from 0.1 to 0.5 |

|

| Low quality of the transferred processed products (works, services) for further processing (use) |

from 0.1 to 0.3 |

|

| Failure to provide raw materials, materials, tools, electricity and other necessary resources |

from 0.1 to 0.5 |

|

| Failure to fulfill or untimely fulfillment of the requirements for a structural unit by related units |

from 0.1 to 0.5 |

|

| Irregularity of work due to the fault of the structural unit - the recipient of the Claim |

from 0.1 to 0.5 |

|

Form 3

Tab. 1. List of factors affecting the value of the KET of the employee

|

P / p No. |

Name of Claim |

Mean. KTV |

| Constant overfulfillment of shift tasks and labor standards | ||

| Higher quality of work compared to other workers | ||

| Reduced equipment downtime against established norms | ||

| Employee initiative to prevent equipment and employee downtime | ||

| Combining professions, expanding the service area | ||

| Permanent performance, along with their duties, the functions of the absent worker | ||

| High labor intensity, performance of work of increased danger | ||

| Performing the most time-consuming and complex jobs | ||

| Manifestation professional excellence ensuring higher labor productivity with high quality of work and shorter terms of the assignment | ||

| Saving basic and auxiliary materials, electricity and other resources | ||

| Development and implementation of new projects aimed at improving production efficiency |

Tab. 2. The list of decreasing indicators for the determination of KET

|

P / p No. |

Name of Claim |

Mean. KTV |

| Non-fulfillment or poor-quality fulfillment of production assignments | ||

| Insufficient intensity or systematic lagging behind the general pace of collective work | ||

| Violation of technological instructions, standard requirements | ||

| Unsatisfactory maintenance of equipment and workplace, violation of equipment operating rules | ||

| Violation of the rules of labor protection and production culture | ||

| Systematic non-fulfillment or untimely fulfillment of duties in accordance with their job (work) instructions | ||

| Systematic execution of works with low quality, errors | ||

| Irrational use of raw materials, materials, tools, electricity and other resources | ||

| Increased downtime of equipment due to the fault of the employee | ||

| Insufficient production skills, low level of professional skill | ||

| Systematic failure to meet production standards | ||

| Violation of labor discipline, internal labor regulations, production culture |

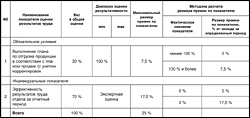

The bonus system in our company assumes both collective and individual remuneration. I would like to dwell on the structure of bonuses (Table 1). Today we use:

- bonus bonuses;

- bonuses for the achievement of key indicators;

- individual bonuses.

Tab. 1. The structure of the bonus system

|

Bonus type |

Bonus characteristics |

||||

|

Bonus indicators |

Criteria for determining the amount of the premium |

A source |

Periodicity |

||

|

Bonus |

Leaders |

Company goals and divisions |

The results of the company |

Profit |

Half year / |

|

Specialists |

Company goals, divisions |

The results of the company |

|||

|

Workers |

Company goals |

The results of the company |

|||

|

Performance Bonus |

Functional management |

Key performance indicators (KPIs) |

Division results |

Cost price |

Quarter |

|

Time-paid workers |

Quarter |

||||

|

Line management |

Month |

||||

|

Individual bonuses |

Piecework workers |

Quality and labor productivity |

Differentiation by occupation |

Cost price |

Month |

Bonus bonuses apply to all personnel of the company - based on the results of half a year / year. The size bonus reward differentiated by size: depending on the increase in sales volume (in relation to the previous year). It is calculated according to a certain formula, which is based on the size of the average monthly rate, the number of tariff rates and a certain coefficient of increase. Compliance with industry standards insignificantly affects the size of the bonus; it depends much more on the achievement of the company's strategic goals. Overfulfillment of the plan also slightly affects the remuneration, since we are not interested in this. Thus, each group of personnel receives "its" bonus, taking into account the level of management, the level of the position and the degree of its influence on the final result.

The distribution of bonus remuneration between departments and individual employees depends on the following factors (Table 2):

- the degree of fulfillment of goals: company, division, individual;